What We're Watching in July

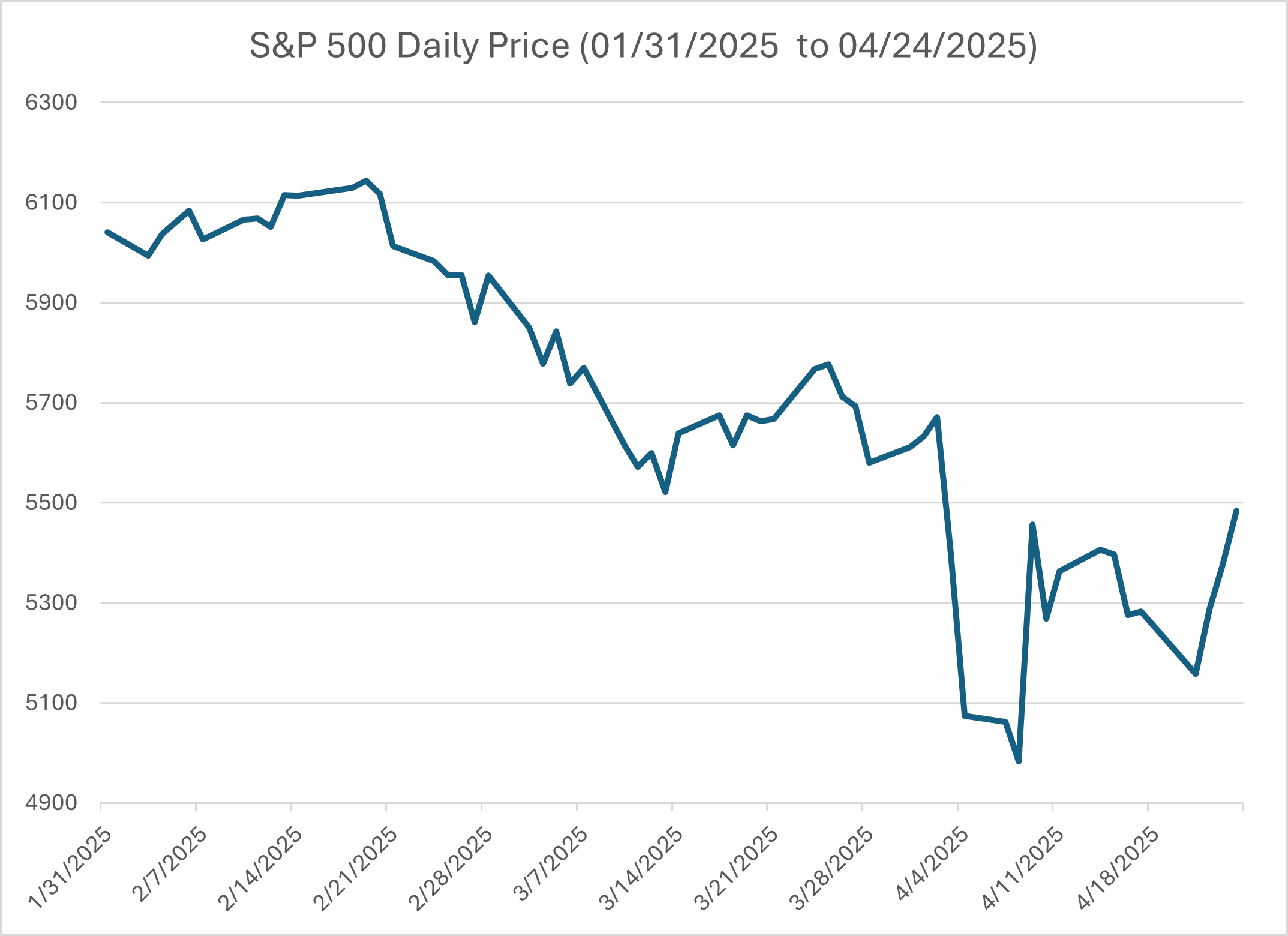

As we enter July and the second half of 2025, markets and the economy remain resilient against a backdrop that feels anything but calm. The U.S. airstrikes on Iranian nuclear facilities over the weekend of June 21–22 introduced a serious geopolitical variable, raising the specter of escalation and potential global conflict. And yet, despite the weight of these headlines, equity markets have moved higher.

.png)