What do you see when you envision your retirement? Are you on a sailboat in the Mediterranean? Baking cookies with your laughing grandchildren? Starting up that small business you were always passionate about? Writing that book like you always wanted? Realizing your dreams requires financial resources and a well-structured plan that optimizes savings and minimizes tax burdens.

Retirement Roadmap

Before we dive into the specifics, it's worth noting that having a documented plan is an important step in saving for retirement. The right plan can serve as a roadmap to guide your decisions and help you reach milestones. It also can act as a shield against distractions arising from market volatility, keeping you focused and objective in your pursuit of retirement goals.

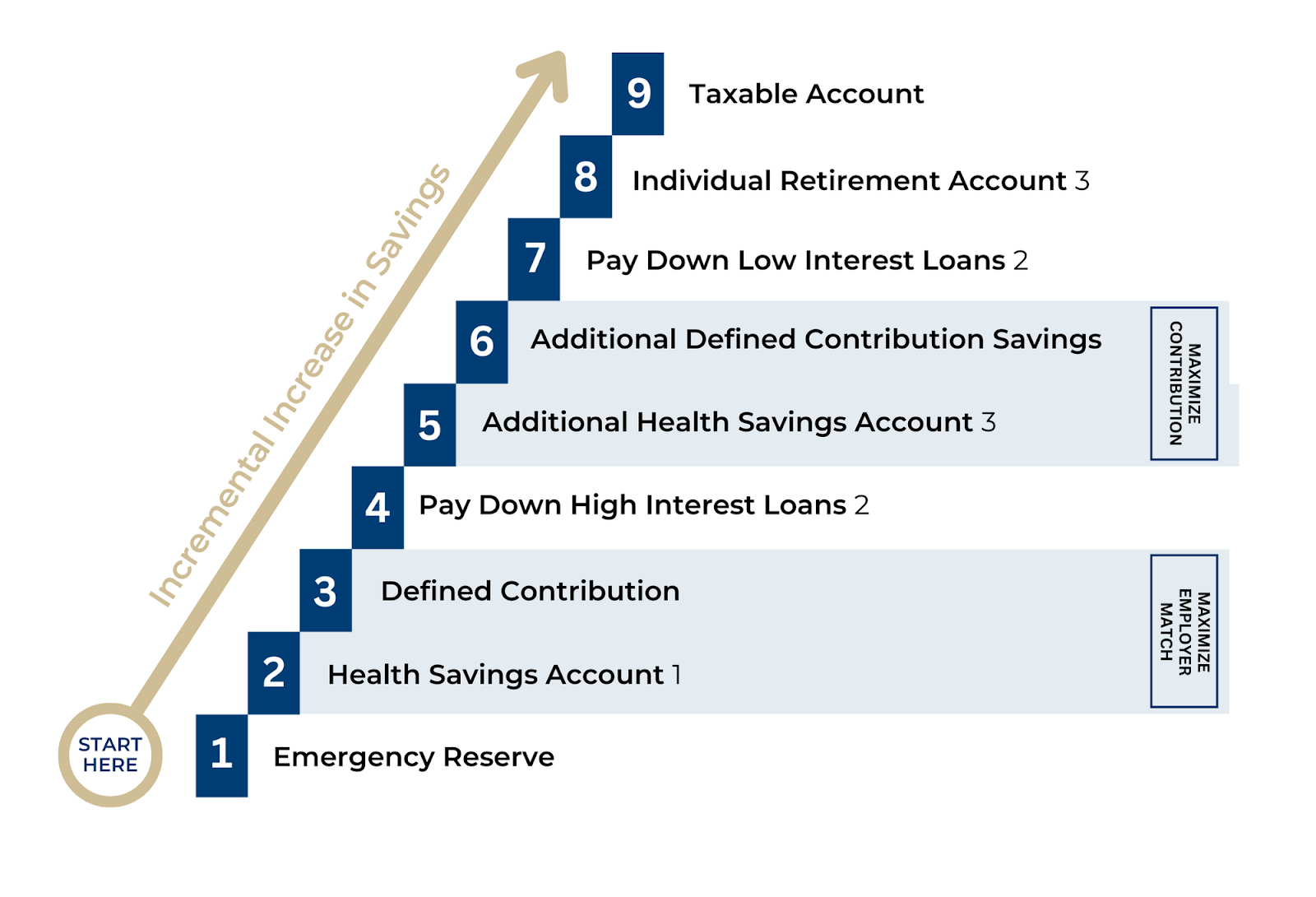

Below is an illustrative retirement savings roadmap designed for investors initiating their retirement plan. This example serves for demonstration purposes only. For crafting a personalized roadmap, it is highly recommended that you consult a registered investment advisor who can tailor it to your specific financial goals and circumstances.

Start with emergency savings to weather spending and income shocks throughout the year and make sure to take advantage of employer matching funds if they are available. An HSA offers triple tax benefits if used for qualified medical expenses in retirement. Prioritize contributions to an HSA before a Defined Contribution plan if current medical expenses can be funded from low-cost sources.4

Source: Source: J.P. Morgan Asset Management analysis. Not intended to be a personal financial plan. For illustrative purposes only.

1 Must have a high-deductible health insurance plan that is eligible to be paired with an HSA. Those taking Social Security benefits age 65 or older and those who are on Medicare are ineligible. Tax penalties apply for non-qualified distributions prior to age 65; consult IRS

Publication 502 or your tax professional.

2 This assumes that a diversified portfolio may earn 7.0% over the long term. Actual returns may be higher or lower. Generally, consider

making additional payments on loans with a higher interest rate than your long-term expected investment return.

3 Income limits may apply for IRAs. If ineligible for these, consider a non-deductible IRA or an after-tax 401(k) contribution. Individual

situations will vary; consult your tax professional.

4 Examples of low-cost funding sources include cash and current income.

In this example, the roadmap starts with building an emergency reserve to provide a financial cushion, ensuring the ability to handle unexpected expenses and fluctuations in income. Once the emergency reserve goal is reached, due to income level, employer matching and insurance benefits, this investor has the opportunities to leverage a Health Savings Account (HSA), a Defined Contribution Plan (DC) and an Individual Retirement Account (IRA).

|

Health Savings Account A HSA is a tax-advantaged savings account designed to help individuals with high-deductible health plans save and pay for qualified medical expenses. |

Defined Contribution Plan A DC plan is a retirement savings plan where contributions from employers, employees, or both determine the final benefit, based on the investment performance of these contributions. |

Individual Retirement Account An IRA is a tax-advantaged investment account that allows individuals to save for retirement with potential tax benefits. Can be either Traditional IRA or Roth IRA. |

Your Time Horizon

Your unique time horizon plays a pivotal role in shaping your retirement plan. Due to the magic of compound growth, the sooner you can begin saving and investing for retirement, the better.

Tax Benefits

The other aspect of compound growth to keep in mind, especially if retirement is still far away, is that even seemingly small tax savings can add up to major differences down the line, which makes it all the more important to pick the accounts that best optimize your savings.

The following descriptions clarify how different account types offer tax benefits.

1. Traditional Individual Retirement Account (IRA)

With a Traditional IRA, contributions are tax-deductible in the year you make them, potentially lowering your taxable income. The earnings then grow tax-deferred until you withdraw them during retirement. A Traditional IRA is an excellent choice to consider if you expect your tax rate to be lower in retirement than it is now. Additionally, it provides a valuable opportunity for tax savings in the present, giving you more funds to invest and grow over time.

2. Roth Individual Retirement Account (IRA)

A Roth IRA, unlike a Traditional IRA, offers tax benefits during retirement rather than at the time of contribution. Contributions to a Roth IRA are made with after-tax money, meaning they are not tax-deductible. However, the advantage comes during retirement: qualified withdrawals, including earnings, are entirely tax-free.

A Roth IRA is worth considering if you anticipate being in a higher tax bracket during retirement. Additionally, Roth IRAs have no required minimum distributions (RMDs), providing more flexibility in managing your retirement income.

3. 401(k) Retirement Plan

A 401(k) is an employer-sponsored retirement plan (a 403(b) plan is a comparable plan for those who work for schools or certain charities, while a 457(b) plan is for those who work for local or state government). Like a Traditional IRA, you can contribute a portion of your pre-tax salary to your 401(k), reducing your taxable income for the current year, and contributions grow tax-deferred until you withdraw them during retirement.

What makes a 401(k) plan stand out from other retirement accounts is that employers often offer a matching contribution. This match is essentially "free money" for your retirement savings. Taking full advantage of the employer match can significantly boost your retirement fund.

4. Roth 401(k) Retirement Plan

Similar to the Roth IRA, the Roth 401(k) offers tax-free withdrawals during retirement. The main difference is that the Roth 401(k) is an employer-sponsored plan, combining the benefits of a traditional 401(k) with those of a Roth IRA.

Contributions to a Roth 401(k) are made with after-tax money, but your earnings grow tax-free and are not subject to taxation upon withdrawal. If your employer offers a Roth 401(k) option, it can be an excellent choice, especially if you expect your tax rate to be higher in retirement or if you desire tax diversification in your retirement accounts.

5. Health Savings Account (HSA)

You may not think of a Health Savings Account (HSA) as a retirement account, but it’s actually one of the most tax-efficient retirement savings vehicles. HSAs have a triple tax advantage: contributions can be made with pre-tax dollars, contributions grow tax-free and withdrawals can be made tax-free for qualified medical expenses. If you’re able to pay your current healthcare expenses out of pocket, you can then use your HSA as another tool to save for retirement.

6. Simplified Employee Pension (SEP) IRA or Solo 401(k) Retirement Plan

What if you’re self-employed or a small business owner? In this case, you may want to consider either a Simplified Employee Pension (SEP) IRA or a Solo 401(k).

With a SEP IRA, you can contribute a percentage of your income (up to a specified limit) as both the employer and the employee. Contributions to a SEP IRA are tax-deductible, providing immediate tax benefits. The earnings in the account grow tax-deferred until retirement.

The Solo 401(k), also known as the Individual 401(k), is designed for self-employed individuals and business owners with no full-time employees (excluding a spouse). This retirement plan offers higher contribution limits than traditional 401(k)s or IRAs, allowing for more significant tax-deferred savings. Solo 401(k)s also provide the option for a Roth component, allowing for after-tax contributions with tax-free withdrawals in retirement.

Key Takeaway

Leveraging a roadmap that guides you to use the right retirement account at the right time is a critical component of your financial health and will significantly impact your future. Each retirement account option comes with its unique set of advantages and considerations, making it essential to evaluate your financial goals, tax situation and individual circumstances.

Consulting with a financial advisor to gain personalized guidance on which retirement account aligns best with your objectives can help you achieve the retirement of your dreams. Contact us today to learn more.